Raising Finance: Identifying the right investor for you and your business

Raising Finance: Identifying the right investor for you and your business

The pandemic has thrown out a variety of new challenges for entrepreneurs looking to grow and scale their business. While raising finance has always been a complex process, the impact of COVID-19 has presented several new challenges. Accordingly, preparation for an investment exercise has never been more important in maximising the chances of a successful outcome.

One of the most important aspects of preparing to raise funds is identifying the right type of investors to approach. There are numerous factors to consider ensuring a good match between your investment objectives and the criteria of said investors. These include: the stage of your business in its lifecycle, how much you are looking to raise, what the investor brings to the table (e.g. capital, strategic infrastructure and/or access to their network). Equally important on top of these factors is that the investor shares your vision and ambition for the growth of the business.

The reality is - not all investors will be a great fit for every business, and whilst capital alone can be luring, business owners should consider exactly what they are looking for in an investor to determine who would be best suited. In this short piece, we will examine some of the most common (equity) investors for businesses thinking about raising finance for growth.

Friends and Family

Most businesses will obtain financing from their own network in the very early days. Typically, these are personal connections (e.g. friends and family) willing to invest small sums of their own personal finances. While often providing easy access and a strong likelihood of deliverability, this group often lacks value-add in terms of commercial and growth benefits.

Angel Investors

Angel investors are typically approached by early-stage businesses that have never run a formal investment process before. They are high net worth individuals who can offer advice and connections and can be more flexible in their approach than more institutional investors. In addition to individual investors, there has been an increase in angel groups, which are groups formed by several angels to make investments.

Crowdfunding

Crowdfunding is a popular way for many early-stage businesses to raise finance as not only does it result (if successful) in money into the business in question but also provides excellent public exposure. While it certainly has its benefits, crowdfunding does not come cheaply, with many platforms requiring a certain level of funds to be committed before they will list the opportunity (often up to half!).

Family Offices

A family office is a private Investment vehicle responsible for investing assets on behalf of either one wealthy family or multiple families. Family offices are typically associated with attributes such as being able to invest at speed without the usual milestones involved with a VC. The backing of a wealthy family can provide substantial networking opportunities.

Venture Capital

Venture capital (VC) is a form of private equity investment for early-stage businesses, demonstrating strong, long-term potential for growth. Whilst VCs range in what stage of the business lifecycle they will invest, it is most common they will participate in Series A, B and C rounds (once the business in question has developed a track record and is seeking more meaningful investment to scale).

Corporate VC

Corporate VC is where large firms take an equity stake in small businesses, where they may also leverage the parent company’s assets to help propel growth. The aim of these types of investments is to help the corporate firm establish a competitive advantage, and they are becoming more and more common, especially with rapid advancements in technology driving the need for innovation.

Having reviewed the landscape, owners should re-examine the attributes they look for in an investor to identify the value-add that matters to them. Asking important questions such as “do I need external support”?, “how will an investor help me grow?”, “Does the investor know the industry?, “Do they have a record of adding value” and “will they understand my business needs”? are key to understanding who to choose. Researching the investors in question in terms of other investments they have made can also help determine many of these responses. These questions will likely vary from business to business but will allow business to prioritise exactly what they are looking for and need.

Despite the impact of COVID, investment appetite has rebounded and is only expected to increase in the months to come. If you are considering raising finance, now is a great time - just ensure you are adequately prepared for the process and know the type of investors you want to pursue. If you would like to explore your options and are thinking about raising finance soon, chat to us today - we would welcome an exploratory chat. Click here to book a call or email us at info@blueboxvelocity.com.

A Day in the Life of an Intern at Bluebox Velocity

A Day in the Life of an Intern at Bluebox Velocity

Ever wondered what it’s like to be an intern at Bluebox Velocity? Find out from Charlie Sullivan, one of Bluebox’s most recent interns. We get to know a bit about Charlie, how he landed the internship, his experience working as an intern at Bluebox Velocity and some advice for university students contemplating work placements.

1. What was your background prior to interning at Bluebox Velocity?

I am a junior finance major at Providence College, from Madison, Connecticut, USA.

2. How did you land the internship?

I landed this internship through Arcadia University, the study abroad program I am currently apart of. I was put in contact with Tracy Kingsnorth who conducted an interview with me back in July. Soon after I received an offer to join the team for the semester.

3. What does an average day/week look like for you?

I have been learning the ropes from Cormac Molloy, one of the Research Analysts, who has shown me how to begin the process of finding the ideal investors, buyers or sellers based on a client’s criteria. I have mostly assisted on projects where the client is looking to raise funds and have therefore gained a real understanding of the in-depth research needed when sourcing the right investors for a client. Week-to-week, based on the timing of a client’s approach to Bluebox Velocity, I assist Cormac with a deep dive into all the information we get from a client, ensuring we know the exact criteria of investor they are looking for. We then begin researching credible investment firms or individual investors who could be potentially interested in this new opportunity via Bluebox Velocity’s extensive databases and platforms, as well as through connections the company has. Once the investor list is compiled, the client company will often need an enhanced prospectus and executive summary drafted for them, so this is also an area I have been exposed to and have had a hand in developing. As of recent, I have been sitting in on some outreach to potential investors. Once outreach is done, given a response from investors, Bluebox Velocity will provide interested investors with the enhanced prospectus or executive summary. That’s when Bluebox Velocity hands over further discussions to the client and completes the deliverables. The progression of my work doesn’t always line up like this as it can vary based on workload and what the team needs assistance with at a certain point in time.

4. What do you wish you’d known before you started?

That work isn’t actually dreadful… it’s… fun…

5. Has the pandemic created any difficulties for you during the internship?

If anything, the pandemic has made it more fun. As the work I do is all computer-based, there is no pressing need to be in the office. Given I am only in London for three and a half months, I use the opportunity of virtual work to boost my exploration of London. I’ve made it a mission to discover the hidden gem coffee shops, see the modern museums, and certainly the historical pubs. Whether it’s Aquila Café on City Road, the courtyard of the V&A museum, or The Old Bank of London, I’ve been able to call those spaces my office for the day. I am immensely grateful to not only be working – but be working in such a vast and cultured city.

6. Do you feel the internship has helped you develop practical skills and what aspect of your internship have you enjoyed the most?

Yes, how to break out of yet another comfort zone. You can’t extend your comfort zone if you are resistant to anything new. As happened with the start of high-school, and then the start of college, the start of your first job is no different. Nerves are high and expectations [can be] low. It took all of one day (in the real office) for me to adapt to my new environment. I think it’s extremely important to be willing to be vulnerable and prove you are there not only to help, but also to learn.

Although I enjoyed the flexibility of hybrid working, what I found most fulfilling was actually going into the office. The reason being comes from my belief in the culture Blubox instils.

7. How do you find the work culture at Bluebox Velocity?

Small offices are to my preference, no one is a clone-trooper of someone else. This means everyone’s opinion, voice, and work matter, regardless if you’re the CEO or just the international intern.

8. What opportunities do you feel you have gained from interning at Bluebox Velocity?

Practical finance knowledge and credible software skills and application.

9. What advice would you give to anyone thinking about joining Bluebox Velocity as an intern?

Ask yourself why you want this. When you figure out the answer, be happy. You’ve figured out your benchmark, or your working goal. Now go achieve it.

Rapid Fire:

- Who was your favourite mentor at Bluebox (you don’t have to say Cormac ;)) Cormac of course. He is the reason I am comfortable to be wrong, and work to be right.

- If you could have one superpower, what would it be? To be able to speak to animals.

- Dream job one day? One day I would like my experience, my character, and my vision to put me in a position where I hold a form of public office.

- If you could have dinner with anyone, dead or alive, who would it be? Jesus

Entrepreneur Interview: Guillaume Kendall of Zedosh

Entrepreneur Interview: Guillaume Kendall of Zedosh

We had the pleasure of getting to know, Guillaume Kendall, Founder and CEO of Zedosh, a seed-stage fintech building the rails to redefine the $400Bn digital advertising market. Their Attention Exchange® engine uses Open Banking and machine learning to connect financially relevant consumers to brands who pay the consumer (rather than big tech) for their attention to video advertising. Zedosh is the marketplace for the Attention Economy.

We chat to Guillaume about how the business started, what makes it unique in the market, as well as his hopes for the future of the business. Guillaume also shares some pointers for entrepreneurs thinking about starting their own business.

- What was your backgrounds prior to setting up Zedosh?

My career has been spent working in sales across several leading technical advisory / consultancy business focused on the Fintech sector. My last role before going ‘all in’ on Zedosh was working with a leading UK bank on the implementation of open banking APIs.

- How did the idea of Zedosh come about?

I’ve had lots of ideas but Zedosh is the only one that kept getting better the more I thought it through. I was on Instagram and kept noticing the same ad appearing time and time again. It was from Patch Plants, and I was already a (rather good!) customer of theirs. It became increasingly frustrating on two fronts. Firstly, it was pointless, wasted advertising that was interrupting my browsing and negatively affecting my feeling towards the brand and secondly, I expected more considering the amount of data I know I’m giving to Facebook. It struck me that if Patch Plants were able to advertise to consumers based on banking transactions and not cookies/tracking pixels, they might have left me alone for a while or maybe communicated something more personal, like ‘thank you, here’s a free pot’.

As time went on, Facebook found itself in increasingly hot water about its use (and abuse) of data and the ethics of its design and business model. The Netflix documentary The Social Dilemma followed the Cambridge Analytica scandal and preceded the most recent ‘Facebook Leaks’ which confirmed that Facebook knows full well the harm it’s causing to our online and real-world communities. Brands are looking for an alternative model.

Open Banking provides the opportunity to re-direct the billions spent supporting Facebook’s proliferation of inefficient marketing funnels, misinformation and hate into the consumer’s pocket instead. We live in an attention economy after all.

- What was most challenging about starting your own business?

Figuring out how to move my idea off a PowerPoint slide and into consumers’ hands! Of course, it comes down to funding and as a first-time entrepreneur, I was surprised by the huge variety of options available, especially if you’re willing to part with half your equity! Luckily, my fiancée is a corporate lawyer and so I was able to navigate carefully through the noise and raise enough via a Convertible Loan Note to build our prototype. In that process, we learnt that what seems straight forward on a PowerPoint slide is less so in code! Specifically, the ability to automate instant micro-payments to our users and overcoming some of Apple’s reservations on our business model. But perseverance pays off and we’ve now made over 3.5k payments to our users via our app.

- What is unique about your business in the market?

The concept of rewarding consumers for their attention isn’t new. However, no one else is considering the underlying value of that attention. Using Open Banking, we’re able to analyse and price the attention of our users. For example, we know immutably the total amount our users spend on coffee, Deliveroo or phone bills every month. If brands want to access that attention market, knowing the exact money value it generates, they should pay for it fairly and transparently, up front. Paying the target consumer is fairer than paying Facebook to interrupt them and makes us cookie and iOS15 proof, which are huge headwinds facing the $400Bn digital advertising market controlled by Facebook and Google.

- What 2 personality traits do you believe make a good business owner and leader?

Empathy and optimism. It’s critical to put yourself in other people’s shoes and see the world from their perspective. Whether they’re team members, prospects, clients or partners, no story is ever one-sided and to build productive relationships, you have to empathise with the other side’s point of view. With regards to optimism, you have to have something that keeps you pushing forward when things aren’t quite going your way! I believe what we’re doing has the potential to democratise the internet and whilst that’s a BIG vision, I’m optimistic about the journey ahead.

- If you had the chance to start Zedosh over again, would you do anything differently?

Not yet, no. Every mistake we’ve made, we’ve learnt from, and I wouldn’t risk getting to where we are today by taking a different path. We’re still right at the start of our journey but very proud of what we’ve achieved so far with limited resources but an abundance of empathy and optimism!

- What advice would you give to a young entrepreneur starting up their own business?

Marry a corporate lawyer! That’s my top tip, but failing that, don’t look back and surround yourself with people smarter than yourself. Starting your own business means you’ll have to wear many hats; just this week I’ve been CTO, CEO and CMO! Bringing on people you trust to get on with things and that you can learn from will relieve pressure and help you grow as a leader - regardless of whether or not the business succeeds.

- Where do you see the business going in the future?

Over the last 3 months, we have been building the engine that matches the right attention to the right content. We’ve called this our Attention Exchange®. The next step for us is to integrate our engine with other 3rd party apps and websites, essentially building the rails for a cookieless, fair and transparent value exchange between brands and consumers anywhere on the web.

- How can firms and individuals, who come across Zedosh, support the business?

We’d love to hear from any B2C brands or media agencies who value the captive attention of relevant consumers. Our average video completion rate is 94% and CTR 16% for content up to 2 minutes long and unlike social media, a ‘view’ for us only counts when 100% of the content has been viewed to completion. With regards to individuals, as long as you have a valid UK bank account, sign up and put your valuable attention to work! Every penny earned is a penny in your pocket instead of Mark Zuckerberg’s.

- Any final words for our Bluebox community?

Thank you for your attention, especially if you’ve got this far! It’s very valuable and I do appreciate it.

Rapid Fire:

- If you could have one superpower what would it be? Time travel

- One person, past or present, you would like to have dinner with? Napoleon Bonaparte

- Three things to take onto a desert island? My fiancée (not sure she’d appreciate that!), nail clippers and Spotify

- Life moto? Say yes more

Contact: Guillaume Kendall, Founder and CEO

Email: Guillaume@zedosh.com

Number: +44 7888710383

If you’re thinking about raising finance for your business and need some assistance, we would be delighted to have an informal and confidential chat to discuss your options in more detail. Book a call via this link or email us at info@blueboxvelocity.com.

The rise of Amazon aggregation M&A

THE RISE OF AMAZON AGGREGATION M&A

By Tessa Trevelyan Thomas of BDB Pitmans LLP

As e-commerce and Amazon have grown rapidly through the Covid-19 pandemic, so too have e-comerce aggregators, leading to a new emerging M&A sector: Amazon aggregation M&A.

Born in the US in 2018 with Thrasio (now reported as being valued at over US$5 billion), Amazon aggregators are spreading rapidly through Europe and worldwide. There are now over 80 active aggregators and the sector has seen significant capital influx – over US$10 billion has been raised by aggregators since April 2020 (according to Marketplace Pulse). Their aim is to acquire and consolidate third party brands selling on Amazon. Some aggregators are now extending beyond Amazon to other online channels such as Shopify and direct-to-consumer (DTC) businesses selling on their own websites. This is a fragmented marketplace with many Amazon FBA (Fulfilment by Amazon) brands being run by young entrepreneurs from their spare room or keen to move on to their next challenge. Amazon aggregators bring quick access to an exit and money for the sellers of a brand and in turn seek to maximise profits through consolidation of brands by creating efficiencies in supply chains and marketing, boosting sales and expanding the reach of each brand.

From our experience with Amazon aggregation M&A, here are seven key points to consider when embarking on buying or selling an Amazon brand:

Speed:

These deals tend to be run on a speedy timeline, with 45 days being the market norm for the period from heads of terms to completion. Amazon aggregation M&A is faster than a standard M&A process, but Amazon aggregators are increasingly experienced and capable of efficient processes against a background of increasing competition.

Valuation:

Amazon FBA businesses are usually valued on a multiple of the last twelve months SDE. EBITDA (earnings before interest, taxation, depreciation and amortisation – a more standard valuation for M&A) is often used on larger deals. SDE instead is seller’s discretionary earnings – this is generally the average net profit of the business over the last twelve months plus any “add backs”. Add backs vary from deal to deal and are subject to negotiation but are generally business expenses that are of a personal benefit to the seller, such as the seller’s salary, pension contributions, health benefits, travel and other seller discretionary expenses. Multiples in this space started as low as 2x but the increasing competition has been driving them up quickly. Factors such as the age of the businesses, strength of the brand, product range, growth potential and risks of the brand will affect the multiple that aggregators will be willing to pay. Sellers should consider whether they need corporate finance advice to get the best valuation.

Deal structure:

Asset deals are the norm for Amazon aggregators in the US – this means the aggregator only buys the assets of the business, such as the stock, brand, intellectual property, trademarks, contracts, Amazon and other online accounts and website. The aggregator does not buy the shares in the business. However, share deals are the norm in the UK because they are more tax efficient. A share deal allows a UK seller, subject to certain conditions, to make use of Business Asset Disposal Relief (formerly Entrepreneurs’ Relief) thereby reducing the rate of capital gains tax (CGT) to 10% on the first £1 million of the seller’s lifetime gains. There is much speculation that CGT rates may change imminently both in the UK and the US which could affect the structure of these deals, although the UK’s recent October budget did not change UK CGT rates.

Consideration:

As with most deals, sellers want cash, ideally upfront at completion. Most commonly, these deals will involve a completion payment and a separate payment for inventory as at completion. There is often a stabilisation or stability payment twelve months post completion if the brand performs in line with agreed expectations. Earn-outs are also common, particularly where there are risks and uncertainty in the business model (e.g. the impact of the pandemic on sales or supply issues) or if the seller remains involved with the brand post-completion. An earn-out is usually paid over two or three years post completion and depends upon the brand’s performance in that period. Consideration shares (with equity being offered to the seller in the holding company or acquisition vehicle) are now becoming more common.

Due diligence:

As with any M&A deal, due diligence is the first major step once basic deal terms have been agreed. Through a data room and a series of DD calls, Amazon aggregators will cover the standard areas in their due diligence (legal, financial/accounting, tax, operational etc) but they will also look closely at the Amazon and brand related issues. DD will therefore also include review and evaluation of information on Amazon Seller Central accounts, traffic and key Amazon metrics, customer reviews (any fake reviews will be an issue), compliance with Amazon terms and conditions (any account suspensions will also be an issue), intellectual property rights and protection, and data protection compliance.

Legal process:

The first step is agreeing a letter of intent – this will include the basic deal terms and price and usually an exclusivity clause (preventing the seller from negotiating a deal with another purchaser) and confidentiality provisions (a separate non-disclosure agreement may also be signed). The key document to the deal in the UK is then the share purchase agreement (SPA). This is usually drafted by the aggregator’s lawyers and will document the transaction and allocate risk between the parties. It will include provisions on price, warranties from the seller on the business, indemnities from the seller on any material issues with the business, limitations on claims that the buyer can make against the seller and restrictions on the seller post-completion (e.g. to prevent the seller from setting up a competing brand immediately post-completion). Other transaction documents include a disclosure letter (containing disclosures from the seller against the warranties) and a service agreement or consultancy agreement (if the seller is staying on with the brand post-completion).

Migration:

The process of migrating control over e-commerce accounts to the aggregator is key to the end of the M&A process. The completion payment will not be released to the seller until migration is complete. On a share sale (as is more standard in the UK), this will be more straightforward assuming all accounts are in the name of the target company. The process is more complex and can take several days or more on an asset deal.

If you are a brand seeking to sell to an Amazon aggregator or an Amazon aggregator seeking to acquire a brand, get in touch with Tessa at tessatrevelyathomas@bdbpitmans.com or Mireille at mireilleturner@bdbpitmans.com.

Alternatively, if you are looking to sell any other type of business you can get in touch with us here or email us at info@blueboxvelocity.com.

November Update

November Update

As the autumn leaves fall from the trees and the air around us becomes icier, our November update comes at a time where there is a great deal of activity, with several topics top of mind. Namely – the state of the UK workforce, inflation and COP26. We have also seen the emergence of new areas of M&A resultant of the pandemic as well as some changes to the M&A procedure which have stemmed from the lockdown, impact of sickness and logistical difficulties. Despite these changes, deal flow seems to be at an all-time high with several exciting things in the pipeline here at Bluebox.

Surprisingly for many, the number of people employed in the UK rose in the month after the closure of the government’s furlough scheme with job vacancies reaching a record high. This general trend has revealed itself within our own business as we are currently recruiting for three new roles to continue on our growth trajectory. The increasing employment rate will most certainly play a large part in guiding policymakers’ interest rate decision when they meet in December. However, other factors will play heavily when deciding on how to deal with the rising inflation rates.

Another point of heated debate is the COP26 summit and whether it actually achieved anything at all. The fact that the summit resulted in a less than satisfactory deal is no surprise, however, many of the agreements made are still a step in the right direction, although can only be judged on their delivery. Rishi Sunak’s promise to turn the UK into “the world’s first net zero-aligned financial centre” has been criticised by Greenpeace UK as being more of a “marketing slogan” than an actual step towards the goal of holding global warming below 1.5C. However, there is evidently money to be invested, with Q3 seeing more capital deployed than in any prior quarter. Ultimately, the financial industry, as well as private individuals, need to align their investments with the Paris Agreement climate goals and should require companies they invest in to establish and communicate a net zero plan. It has become evident that we all need to play our part in unleashing the trillions in private and public sector finance required to secure global net zero.

As we embark on the run up to Christmas, perhaps this is a good opportunity to think about how we could do our part to help limit climate change. Whether that means being less wasteful during the Christmas period by ensuring we throw away less food or gifting in a more sustainable manner, each individual action has an impact. We have decided that the gifts chosen for our secret Santa this year have to either be ethically sourced or follow the WWF’s green Christmas gift guide.

As we near the end of the year, we are excited to see what we can complete before then and we urge you to keep an eye on this space. In the mean time, keep up to date with what’s happening here at Bluebox Velocity via our blog or get updates straight to your inbox by subscribing to our newsletter.

Wishing you all a happy and healthy lead up to the Christmas period.

The Bluebox Team

Entrepreneur Interview - Barnaby Procopiou of Cashero

Entrepreneur Interview: Barnaby Procopiou of FinTech startup, Cashero

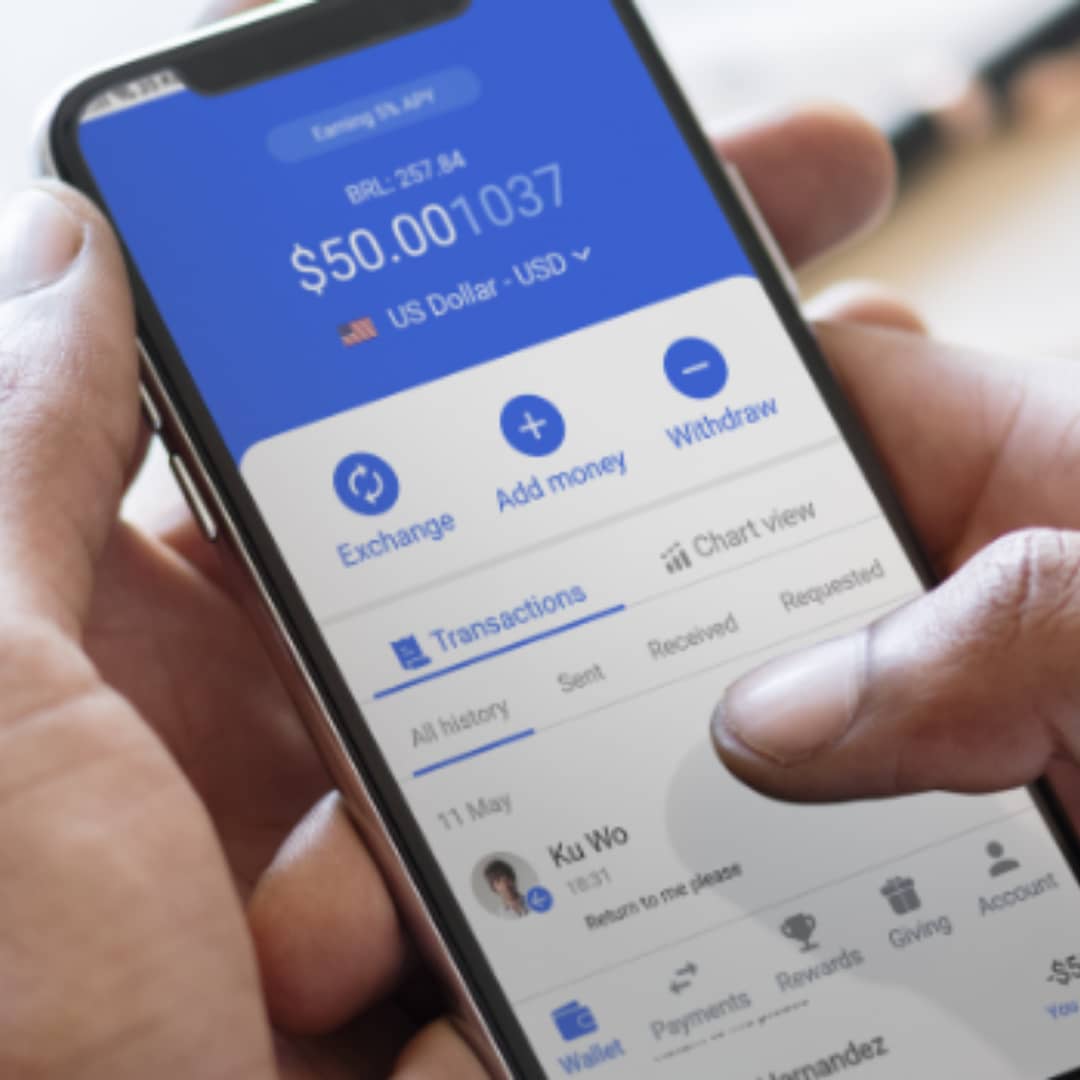

We had the pleasure of getting to know, Barnaby Procopiou, Director, Founding Partner and CFO of Cashero, a FinTech startup blockchain-based payment eco-system, that provides a secure platform for high-yield savings, multi-currency wallets and instant, fee-free internal and cross border payments.

Cashero recognises the appeal and requirement for cash savings but that inflation, high remittance fees and payment friction are a problem for individuals and businesses across the globe. Cashero was founded in 2020 following 2 years of idea conceptualisation, research, iteration and development to solve these problems. They are now in Launch phase and will be available for public use later this year.

We chat to Barnaby about how the business started, what makes this FinTech startup unique in the market, as well as future hopes for Cashero. Barnaby also shares some pointers for entrepreneurs thinking about starting their own business.

- How did the idea of Cashero come about?

The idea of Cashero was born out of the desire to streamline payments for individuals and unbanked individuals across sub-saharan Africa. During 2017, the team spent time across Accra and Nigeria working on potential financial products and tax-based structures to assist the country with outside investment. It was here that the team realised the issues faced by the general public when it came to banking and the onerous charges levied on those using mobile phone-based payment systems that would charge for basic internal transactions and cash withdrawals. Following further research and time spent across African territories, the team realised the problem was systemic and by solving the problem for one African territory the idea could be rolled out across the continent. The conception of Cashero sought to improve the system, allowing users with more volatile currencies to convert to more stable currencies like the pound and dollar, whilst earning interest in those currencies. After many iterations, the team quickly realised the product would not only be useful to unbanked populations across the globe, but also banked and underserved populations across the planet.

- What is unique about your business in the market?

The service is all encompassing and offers reach in 4 key services - instant payments, global remittance, high yield saving and multi-currency wallets/fx. Given that we cross or span these 4 markets, the market size is quite huge at over $29trillion. Whilst there are well known competitors in each of these fields, they tend to focus on 1 or 2 core services, meaning that individuals and businesses often have to use a batch of products or providers to achieve their end goal. Whilst this does make us useful, it does not make us truly unique. What makes us unique is the way we conduct the business. As we have incorporated traditional and well-established financial structures and banking ideology and combined it with new age technology – blockchain, we are able to offer many of these services for free or for a fraction of the cost of our competitors. Therefore, whilst we do have competitors, we are a disruptor in these 4 service fields as we do not rely on the charges of these services to thrive and grow our business and profits.

- How has the Coronavirus pandemic affected the business, and what contingency plans were put in place to ensure survival?

The Coronavirus has affected all businesses globally in some way but not in the way, or ways, that we anticipated. Although legal work slowed with advisors and teams working from home, we noticed an increase in e-commerce business, transaction volume and mobile payments over the period. Interestingly, the last 24 months have also been very interesting for the blockchain and crypto currency space with more eyes moving to this newly developing marketplace. Given that our product and service offering spans over 120 territories, assisting with the spread of risk geographically, events like US elections, Brexit and Covid take little effect on our momentum. Furthermore, as people have worked from home and relied more so on internet-based platforms and mobile phone services, we believe this pushes Cashero to be the right product at the right time.

- What two personality traits do you believe make a good business owner and leader?

Belief and sound business ethics. Understanding and clearly defining the core elements of the business has allowed the team and I to cultivate a clear belief and direction for the business. With the business and service offering defined, a leader can (and must) establish a clear and focused commitment to the project and always protect business conduct and ethics: Lead by example and start as you mean to go on. There are hurdles, delays and challenges with every new business so it is easy for doubt to set in, eyes to move to an ‘easier route’ or better offers to land on the table. Belief and sound business ethics will keep new projects and innovators on the right track to build something that will stand the test of time.

- If you had the chance to start Cashero over again, would you do anything differently?

This is a good question. I think that we have stayed true to our course and in ‘downtime’ periods we have focused on improving and refining our offering in order to advance, develop and test our product. One could argue that the product could have been launched earlier had we focused on the crypto market and crypto users. Whilst this would have fast tracked profits, I believe this would have shortened our lifespan and our remit. A move like this may have also alienated regulators and banking partners later on down the line.

- What advice would you give to a young entrepreneur starting up their own business?

Try and define your vision as clearly as possible and understand that progress each day, no matter how small, is still progress. Entrepreneurs should enjoy the journey and as corny as it sounds - learn to ride the wave - because along the journey your idea may be adapted or improved by new knowledge, feedback, criticism or market movements.

- Where do you see your FinTech startup going in the future?

Our first priority is to launch. Once we launch, we will look for strong partners with established user bases to catalyse the user acquisition forecasts.

- How can firms and individuals, who come across Cashero, support the business?

Simply by opening an account and spreading the word.

- Any final words?

I hope I have provided a helpful insight into our business and who we are. If you are interested in finding out more, investing in our vision or becoming a partner, we are open to support and innovative ideas or partnerships.

Contact: Barnaby Procopiou - Director, Founding Partner, CFO

Email: bp@cashero.com

Number: +44 7814 756226

If you’re thinking about raising finance for your business and need some assistance, we would be delighted to have an informal and confidential chat to discuss your options in more detail. Book a call via this link or email us at info@blueboxvelocity.com.

The Impact of Covid-19 on Acquisitions

The Impact of Covid-19 on Acquisitions

Tracy Evans, Legal Director at EMW Law LLP, explores how the impact of Covid-19 was seen in the merger and acquisition (M&A) process. In this article, she reflects on the challenges that their clients and team faced in light of the pandemic when dealing with share and business sales and acquisitions. The lockdown, impact of sickness and logistical difficulties all culminated in some changes to the M&A procedure. In this article, the themes of due diligence, negotiating the deal structure, drafting the purchase agreement and the deal timetable will be discussed in terms of the implications of Covid-19 on Acquisitions.

Due Diligence

In order to identify key commercial or legal risks, the potential buyer of a target company will often conduct due diligence. We have found that Covid-19 has not only perpetuated existing risks but also presented new risks. For example, when a buyer is looking to purchase a company, it will now want to analyse the effect that Covid-19 had on the business, whether the company has sufficient emergency processes in place and how prepared the company is to suffer another crisis in the future. Therefore, the impact of Covid-19 on Acquisitions in terms of the due diligence process has been quite evident. Whilst every transaction is unique, we have identified particular areas that may require enhanced due diligence in the post-lockdown world these include:

- Employment – for example, whether employees were furloughed, how the target handled employee absences during the pandemic, compliance with changing employment laws and measures taken to protect employees;

- Data protection/GDPR risks – due to the change to remote working, the buyer will want to establish what systems the target had in place to ensure that they were compliant with GDPR; and

- Exposure to supply chain disruption – depending on the type of business of the target, they may be involved in a supply chain. The unpredictable nature of Covid-19 meant that certain businesses suffered considerably, and this had a huge impact on those businesses further down and also higher up in the supply chain. The buyer will want to establish that the target has been able to meet its obligations to its customers.

Negotiating the deal structure

It seems Covid-19 has had an impact on how sellers and buyers deal with pricing structures. Pre-Covid-19, it was common practice for share purchase transactions to proceed on the basis of a locked box mechanism; which involves agreeing a fixed price for the sale shares prior to the acquisition being finalised on a recent set of accounts of the target. It was evident to us, particularly at the start of lockdown, that buyers were hesitant to proceed with a locked box mechanism, particularly where the balance sheet had been prepared pre-Covid-19 thus likely to not give an accurate reflection of the value of the target. We found that buyers and sellers were agreeing to use a completion accounts mechanism; which values the target at the date of completion ensuring that the seller retains the economic risk of the target until completion.

Drafting the purchase agreement

Whilst the need for heightened warranty protection due to the impact of Covid-19 varies from business to business. We have been mindful and will continue to be of the following areas of warranty protection that may need to be heightened when acting for a buyer.

- The situation with regards to material contracts, particularly whether there have been any breaches in performance;

- The status of the target’s relationships with suppliers and customers including delayed orders and relief from or default on payment terms;

- The adequacy of the target’s IT systems, its exposure to data privacy and cyber risks resulting from Covid-19 related changes in working practice;

- Collectability of book debt;

- Compliance with laws introduced to manage Covid-19;

- The target’s take up of available government Covid-19 assistance or financial support packages; and

- Exposure to claims under employment laws, including those arising from implementing furloughs, redundancies and changes in work requirements.

Deal timetable

We have also seen an impact on the deal timetable as a result of Covid-19. The various areas can be split into the following categories:

- Due diligence process – this process, in not every deal, but a few has been lengthier where access is required to obtain physical documents or where a physical inspection of plant/machinery/buildings was required.

- There have been delays in obtaining regulatory clearance in some transactions and disruption to the filing process – with widespread office closures, staff absence, and operational disruption.

- Shareholder and board meetings – during the pandemic is was very difficult (if not impossible) for meetings to be held in person. Therefore, most of these meetings were held online.

- One area where Covid-19 has increased efficiencies is electronic signing; which was used pre-pandemic occasionally but it is now used almost without question in every deal.

In conclusion, the impact of Covid-19 on acquisitions is evident as this article has summarised some key impacts that we have witnessed on the M&A process due to Covid-19. Undoubtedly, this is not an exhaustive list of effects and we will no doubt be analysing further effects of Covid-19 in this regard for the coming years.

If you are in need of assistance for your M&A process, feel free to get in touch. We would welcome an introductory chat to see if we could help. Get in touch with us here or email us at info@blueboxvelocity.com.

Top Tips for Preparing Your Business For Sale

Top Tips for Preparing Your Business For Sale

Selling a business is often the most important ‘transaction’ in a business owner’s life. Below we outline some top tips for preparing your business for sale in order to increase your chances of success.

Tip 1 - Setting your objectives

Misalignment of objectives between shareholders is a key reason many sale processes fail. You (and your other shareholders) must consider what you are looking to achieve from the exercise before getting started. Setting objectives involves more than simply agreeing on what value you are happy selling your business for. When are you looking to sell? What percentage stake are you looking to sell? Are you looking to have an ongoing role? If so, for how long? Is there anyone in the business that should be looked after following completion of a deal? These are only a few of the financial and non-financial questions you should ask yourself. It is critical you fully identify your objectives when preparing your business for sale as these will ultimately shape your exit route and the types of buyers you speak to.

Tip 2 - Health check your business – get rid of any skeletons in the closet!

It is a sad fact that over 90% of all businesses ‘taken to market’ fail to sell. One of the main reasons for this is that there are ‘skeletons in the closet’ that are unearthed late in the due diligence process. To protect against this, and to give yourself the best chance of achieving a successful exit, you should review key areas of your business such as intellectual property, employment, health and safety and tax to check against any material issues that may arise.

Tip 3 - Prepare a list of potential buyers

Before you “go to market”, you first need to identify the buyers you are going to speak to. The list of buyers will heavily depend on your objectives for the exercise and your chosen exit route. In many cases, dual-track processes can be run whereby strategic and financial investors are contacted, and multiple exit routes are explored. Determining your list of buyers is probably the most important element of any sale exercise. Not only do you need to identify buyers who are likely to have interest in buying your business, but they also need to have an ability to pay. The latter, particularly in the SME space, can be challenging; often the relevant information is not disclosed publicly. Corporate finance advisors will use a host of resources to reach a conclusion on this and prepare a qualified list, such as databases and leveraging their networks.

Tip 4 - Put together all marketing materials

Another key element when preparing your business for sale is to compile a mini prospectus or teaser, this is a short document that is sent to your buyers when first approached. Whilst it may be brief, it should contain sufficient information about your business (what it does, what makes it special and headline financials) to stimulate initial interest. If potential buyers are then keen to find out more, you should ask them to sign a Non-Disclosure Agreement (NDA), meaning they agree to keep the process confidential, as well as any information received.

Tip 5 – Get all your financial information in one place

We recommend putting together a ‘data book’, usually in an Excel spreadsheet – this is a great way to compile financial information about your business to share with potential buyers during the sale process. A Prospectus will contain limited financial information and buyers will need to understand this in more detail before putting forward an offer. Some suggested information a data book could contain is as follows:

- Detailed management accounts

- A reconciliation between management accounts and statutory accounts

- Details of any exceptional, non-recurring costs or revenue to the business (these should be added back or deducted from profit in the year they occur to arrive at a ‘normalised profit’)

- Breakdowns of revenue and gross profit

If you are considering a sale exercise, now is a great time - just ensure you are adequately prepared for the process and know the type of buyers you want to pursue. For a full step-by-step guide to selling a business, click here.

If you're thinking about selling your business, get in touch with us today via this link, email us at info@blueboxvelocity.com or call +44 (0)203 924 5150.

Entrepreneur Interview - Nick Ball, Managing Director at Impact

Entrepreneur Interview - Nick Ball, Managing Director at Impact

This month we had the pleasure of getting to know Nick Ball, Managing Director at Impact Air Systems - global waste extraction and separation specialists. Nick shares some valuable information about his experience of the M&A process as well as gives some tips to entrepreneurs considering a sale. We also learn about his journey to Managing Director and his hopes for the future of the business.

1. What is your background prior to becoming Managing Director at Impact Air Systems?

I have only ever worked at Impact Air Systems. I started as a van driver as a holiday job in 1994, was asked to consider a role as a junior project engineer instead of going back to college, which I took and then worked my way up through the project and sales team to general manager before being given the opportunity to buy the business in 2007.

2. How has Impact Air Systems evolved since you bought out the business?

When we bought the business in 2007 we were primarily working in waste and trim from production machinery but as recycling started to take off in a big way we got involved in using air to separate waste in the recycling industry itself and that catapulted us into a whole new market which escalated and allowed us to create some machine based solutions instead of the traditional bespoke system solutions we were used to.

3. Sustainability seems to be increasingly more important to business owners, have you noticed a greater uptake in air-based solutions to move and separate waste in the last 5 years? Can you comment on how your systems are improving sustainable practices?

There has certainly been an increase in interest in our solutions over the last 5 years although I can’t honestly say that from a customer’s perspective it is with sustainability in mind, it seems to be the value of the recyclable materials that can be recovered that drives interest more than a moral responsibility. That said, our density separation systems provide an efficient way to refine the recyclable content and prevent unnecessary material going to landfill, thus improving sustainable practices.

4. How has the Coronavirus pandemic affected the business, and what contingency plans were put in place to ensure survival?

We have been very lucky to be largely unaffected by the pandemic, we had a little time when we couldn’t get engineers into customer’s sites to survey or maintain but as soon as industry starting moving again we resumed business as usual. We are very lucky to work in packaging and recycling and as everyone was at home ordering items that are delivered in boxes that were then recycled, our core customers were as busy as ever.

5. Impact has recently been acquired by ADDTECH, how did you find the M&A process? What were the biggest challenges you faced during the process and how did you get past them?

Our whole M&A process took place during the pandemic which was a challenge in itself as it meant that all meetings took place over Zoom. Building a rapport was difficult and relying on internet connections from home was problematic with the whole family at home. We were very lucky to be able to get one face to face meeting for a couple of hours at the airport. Apart from that I’d say the two biggest problems we faced were keeping the whole process a secret from all staff which was extremely difficult as we are a very open company and everyone knows where I am at all times and the amount of work involved in the due diligence phase to provide all of the answers to the tireless solicitors. Despite the fact that we have very well organised documentation for all aspects of the business I couldn’t have provided all of the answers without the help of our Accounts Manager and Business Systems Manager.

6. What three tips do you have for business owners looking to sell their business?

- Use a reputable company to help you, don’t think you can do it by yourself.

- Don’t underestimate the time and effort involved in the process and how distracting it can be.

- Be very clear on why you’re doing it and what you are going to do after.

7. Post deal, you remain at Impact as Managing Director, where do you see the company going in the future?

Impact has lots of opportunity to grow and improve its market presence around the world in a number of sectors including metal packaging and with the support of our new owners I look forward to pursuing these new opportunities. In the last few years are work in the United States had really started to ramp up and I’m looking to see that grow post pandemic.

8. What 2 personality traits do you believe make a good Managing Director?

- The ability to see situations from different perspectives.

- The ability to keep calm and level headed in stressful situations

9. What advice would you give to a young entrepreneur starting up their own business?

Keep your eye on the numbers, it is so easy for a great idea to run away with itself, you have to keep a constant check that it is going to be profitable. Listen to as many podcasts and mentors as possible to learn from other people’s mistakes, there is a lot of advice out there if you take the time to look for it.

Rapid Fire:

- If you could have one super power, what would it be? To stay young

- If you could have dinner with anyone (past or present) who would it be? My late Grandpa, he would be so proud of what I have achieved.

- Go to holiday destination? Maldives

- If you could only eat one dish for the rest of your life, what would it be? Chicken Mushroom & chips with a bit of curry sauce (and maybe a slice of bread and butter).

If you’re thinking about selling your business and need some assistance, we would be delighted to arrange an informal meeting (over Zoom or Teams) to discuss your options in more detail. Book a call via this link or email us at info@blueboxvelocity.com.

Meet the Team: James Jackson, Head of Sales

Meet the Team: James Jackson, Head of Sales

This month we interview our Head of Sales, James Jackson. We sat down with James to get to know him a bit better, why he chose his role at Velocity and a bit about what he enjoys doing outside of work.

What was your background prior to joining Bluebox Velocity?

I began my career working in sales for some of the world’s largest MedTech companies. After a few years I decided to leave the industry and became a negotiation consultant, specialising in negotiation training, coaching and strategy for a leading international firm working across a variety of industry sectors. My most recent venture prior to Bluebox Velocity was my own negotiation consultancy where I used my commercial experience to help create solutions to strategic challenges, whilst delivering bespoke training and coaching programmes for SME clients across multiple sectors.

How do you think your past roles have equipped you with the skills you’ll need for your new role as Head of Sales?

My commercial roles across multiple industries, organisations, teams and functions has given me the exposure and experience required to grasp this role and hit the ground running. My experience in training, coaching and managing teams gives me the confidence to support, build and grow a high-performance sales team. And having worked for myself, I know first-hand the value of the proposition we offer meaning I can fully get behind it to drive growth.

You previously worked as a negotiation expert, what do you believe are the 3 key elements of good negotiating?

Firstly, not all negotiations are the same, therefore understanding the context and having clarity on your objectives is essential, so that you can plan what approach to take. As for the negotiation itself, I would say having control of your emotions is key and not letting feelings of discomfort influence your decision making at any point. – be comfortable with being uncomfortable! Lastly, the power of silence…this can be your strongest tool if used appropriately.

How did you find out about Bluebox Velocity and what were the reasons you wanted to join the company?

I came across Bluebox Velocity on LinkedIn, and it instantly grabbed my attention. After a few meetings with the team, I was really impressed and excited about the opportunity. I was ready and hungry to join a company where I could not only be an integral part of the team that is contributing to the vision, mission, growth and success of the business – but also work alongside some great minds and be part of something that is unique and disruptive in the M&A market.

What is your biggest achievement to date – personal or professional?

Going out on my own and starting a business – one of the hardest things I have ever done but most rewarding at the same time - I learnt a lot about myself too!

Given a chance, who would you like to be for a day?

Tiger Woods in his heyday – especially on the first day of a club championship weekend!

What’s the best advice you’ve ever received?

Some people make things happen. Some people let things happen. Others wonder what the hell just happened! It’s your choice who you want to be!

What is one thing you couldn’t live without, and why?

My family, they are the most important thing to me. And then my golf clubs!

We finish the interview, and you step outside the house and find a lottery ticket that ends up winning £10 million. What would you do?

Firstly, I’d Google if a lottery ticket can be tracked to the purchaser, if not I would then ask my wife for her opinion - my gut instinct, give a few million to charity for my conscience and keep the rest!

Rapid Fire:

- Summer or Winter? Summer

- Favourite cuisine? Italian - love pasta!

- Favourite sport? Golf

- How would your friends describe you? Most himself in a flip flop!